Visa Cash Advance Fees in Betting

The fee that nobody saw coming

Before the credit-card ban came into force, the cash-advance fee was the most expensive surprise in Australian punting. Customers would deposit a few hundred dollars at a bookmaker using their Visa credit card, win or lose at the punt as usual, and then notice on the next month’s statement that the deposit had been classified as a cash advance – racking up a one-off fee, immediate interest at a higher rate than purchases, and no interest-free period. A fifty-dollar deposit could become a sixty-five-dollar charge before the customer had even thought about the bet itself.

The credit ban that took effect on 11 June 2024 has eliminated the trap going forward – credit cards are simply not accepted for licensed Australian wagering deposits any more, so the cash-advance classification is moot. But the historical exposure didn’t vanish. Punters still call me about old cash-advance fees that surfaced months after the deposit, accumulated interest that compounded for years, and statements they didn’t review carefully at the time. The fee is gone but its echoes are not.

This piece is the historical explainer for the trap, what’s still on punters’ statements from the pre-ban era, and what (if anything) you can do about legacy charges in 2026.

Avoid hidden fees by checking our homepage.

Cash advance versus purchase – the classification that hurt

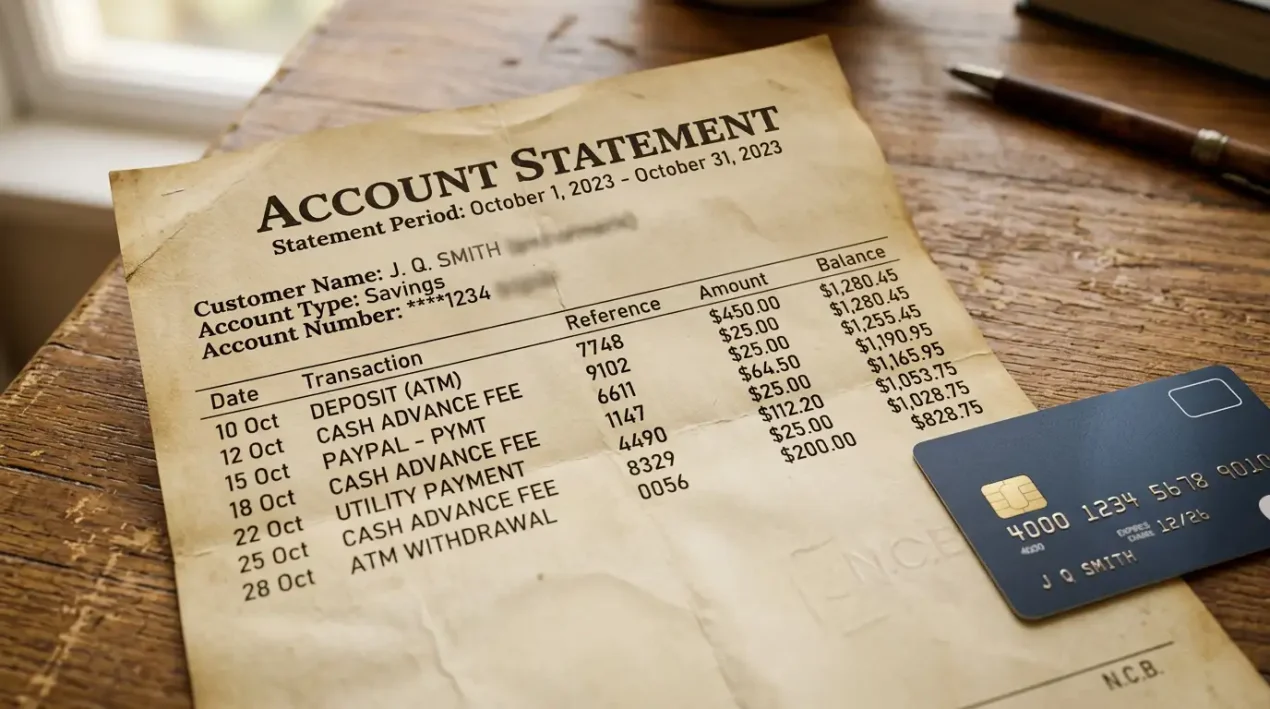

The mechanics of credit-card billing make a sharp distinction between purchases and cash advances. A purchase is what you’d pay for in a shop – clear merchant, normal interchange, interest-free period if you pay your statement off, no separate fee. A cash advance is when you draw cash from an ATM with your credit card or do something equivalent – immediate interest from day one, higher interest rate, a separate up-front fee usually quoted as 3% of the transaction or AU$10, whichever is higher.

The classification depends on the merchant’s MCC and on the issuer’s internal policy for that MCC. Most issuers historically treated MCC 7995 – the gambling category – as a cash-advance equivalent for credit-card transactions. The reasoning was that a gambling deposit is structurally similar to drawing cash: you’re putting money into an account from which you can withdraw cash, just with a wagering layer in between.

So a credit-card deposit at a bookmaker would land on your statement as a cash advance, with the cash-advance fee applied at the moment of the transaction and interest accruing immediately at the cash-advance rate. For customers who paid their card off in full each month and assumed no interest, the surprise on the statement was significant.

Pre-ban bookmaker coding and the issuer’s choice

The frustrating part of the pre-ban setup was that the cash-advance classification wasn’t universal. Two different banks could have treated the same bookmaker transaction differently. Some Australian issuers cash-coded gambling transactions across the board. Others ran a hybrid model where small transactions were treated as purchases and larger ones as cash advances. A third group treated certain operators as cash advances and others as purchases, based on internal risk assessments of the merchant.

This inconsistency was a known headache for years before the credit ban. Industry advocates argued that bookmaker deposits should be treated as purchases like any other merchant transaction. Banks pushed back that the cash-fungibility of a wagering balance made the cash-advance treatment more accurate. Customers were caught in the middle, often discovering the classification only when the statement arrived.

Card-payment value in Australia hit AU$1.1 trillion in 2025, and even before the credit ban, gambling deposits were a small but visible slice of that. The cash-advance fees collected from gambling deposits were meaningful revenue for issuers, which is part of why the inconsistent classification persisted for so long without standardisation.

Interest accrual and how the fees compounded

The headline cash-advance fee was just the first cost. The bigger expense for customers who carried a balance was the interest. Cash-advance balances on most Australian credit cards accrue interest from day one, at a rate that’s typically several percentage points higher than the purchase rate, and there’s no interest-free period regardless of how the rest of the card is managed.

What this meant in practice was that even if you paid your card off in full each month, the cash-advance portion of a gambling deposit accrued interest for the days between the transaction date and the payment date. A AU$500 deposit on the 1st of a month, with the card paid off on the 25th, generated about AU$6 to AU$8 of interest on top of the cash-advance fee. Most customers never noticed the line item; some noticed and wrote it off; a few realised the pattern and switched rails before the credit ban formalised the answer.

Customers who didn’t pay their card off in full each month were in a different category of trouble. Cash-advance balances usually had to be paid down before purchase balances, but the higher interest rate meant the running total compounded faster than purchases would have. A AU$1,000 gambling deposit on a credit card that the customer carried for three months at 21% APR was accruing about AU$50 of interest on top of the original cash-advance fee. Australians lost an estimated AU$31.5 billion across the 2022-23 financial year on gambling overall, and a slice of that loss is the kind of cash-advance interest that wasn’t even part of the wagering itself.

Legacy statements after the ban

The ban took effect prospectively, not retroactively. Cash-advance fees and interest accrued before 11 June 2024 are still owed and still on statements. Punters who closed gambling-related credit-card balances in 2023 are usually clear, but anyone who carried a balance from a 2022 or 2023 gambling deposit through to 2024 might still see the residual interest on a current statement, especially if they’ve been making minimum payments rather than paying down aggressively.

The other lingering effect is on credit reports. Cash-advance utilisation, particularly persistent cash-advance balances, contributes to credit-utilisation ratios that lenders weight when assessing future credit applications. Someone who maintained heavy cash-advance balances from gambling deposits in the 2020 to 2024 window may still see the impact on their credit score in 2026, even though the underlying transactions are no longer legal under the ban.

The compliance picture around the ban itself remains active. ACMA’s 2024-25 enforcement work caught fifty operators with credit-card or cryptocurrency references in their terms and conditions and required all to remediate by 30 June 2025. The fines for credit-related breaches sit at up to AU$247,500 per offence, which has kept operators careful about how they retire any historical credit-card workflows from their systems.

Can old cash-advance fees be reversed?

The honest answer is: rarely, and only in narrow circumstances. The classification of a gambling transaction as a cash advance was contractually permitted by every major Australian credit-card issuer, disclosed in the cardholder agreement, and consistent with industry practice at the time. Asking for a retrospective reversal of a 2022 cash-advance fee in 2026 doesn’t have a strong basis under any standard consumer-protection framework.

The narrow case where a reversal might work is if the cash-advance classification was applied incorrectly under the bank’s own policy. If your bank’s policy at the time treated bookmaker deposits as purchases for amounts under AU$200 (some did) and you were charged a cash-advance fee on a AU$150 deposit, that’s an error you could potentially get refunded. The bank would have to find the error in its own records, which usually requires you to identify the specific transaction and the specific policy that should have applied.

A bank-write-off path exists for customers in financial hardship, where the bank may agree to clear residual interest as part of a broader workout arrangement. This isn’t a retrospective challenge of the original classification; it’s a current hardship process that addresses the present balance regardless of how it accumulated. If you’re carrying gambling-related cash-advance balances that you can’t service, this is the avenue worth exploring rather than trying to dispute the historical fees themselves.

What the ban changed for the future

The credit-card ban makes all of this irrelevant for transactions from 11 June 2024 onward. There’s no scenario under which a 2026 bookmaker deposit can become a cash-advance fee, because the bookmaker can’t accept the credit card in the first place. The trap that defined a generation of credit-card punting is structurally closed.

What remains is the historical exposure, the residual statement entries, and the lessons learned. For customers who came up through the cash-advance era, the post-ban payment landscape is genuinely cleaner. Visa Debit deposits don’t generate cash-advance fees because they aren’t credit. PayID deposits are bank transfers and aren’t classified by any of the credit-card mechanics. The unintended consequence of the ban has been to remove a fee structure that confused punters for years.

Discover how Visa Direct compares to bank transfers for speed.

For the deeper picture of how the credit-card ban itself was implemented and what it changed, my piece on Apple Pay, Google Pay and the credit-card ban covers the broader credit-related-products framework.

Can a 2023 Visa cash-advance gambling fee be reversed retroactively?

Generally no. The cash-advance classification was contractually permitted under standard cardholder agreements and consistent with industry practice. The narrow exception is if your bank’s own policy was applied incorrectly – for example, if it treated certain transaction sizes as purchases but classified yours as a cash advance in error. That’s a refund argument, not a policy challenge.

Did all banks classify gambling deposits as cash advances?

No. Most Australian issuers cash-coded MCC 7995 transactions, but the practice wasn’t uniform. Some banks treated small deposits as purchases and only larger ones as cash advances. A few treated the classification as merchant-specific. Customers often didn’t know which category their card fell into until the statement arrived, which is part of why the cash-advance trap was so persistent.

How can I check if past Visa transactions were coded as cash advances?

Look at the line item on the statement. Cash advances are usually labelled separately from purchases – often with phrases like ‘cash advance’ or ‘cash withdrawal’ – and they show the cash-advance fee as a separate charge alongside the principal amount. The interest applied to cash-advance balances is also reported separately on most statements. If you’re unsure, your bank can pull the historical transaction-level classification from its records.