Visa Betting in Australia: The Complete Guide

Card scheme rules, AU regulators, real numbers — no affiliate spin.

Start Reading

The first time a punter rings me about a "weird Visa decline at Sportsbet", I already know the answer before they finish the sentence. Eleven years sitting between card-scheme rule books and ACMA notices has taught me that most of what punters believe about Visa and betting in this country was true in 2019, half-true in 2022, and largely wrong from June 2024 onwards.

I started writing this guide because the search results have not caught up. Plenty of pages still tell you to "use your Visa credit card to top up your account fast", which is, as of the federal credit-card ban, simply illegal for licensed Australian wagering operators to facilitate. Card scheme rules did not change. Australian law did. That one regulatory hinge has rearranged everything around how Visa moves money into and out of a betting account.

AU$247,500

Maximum penalty per breach of the credit-card prohibition for an Australian wagering operator.

AU$1.1 trillion

Total card payments value in Australia in 2025, with Visa carrying the majority of online spend.

134

Active online wagering services operating under Australian licences in April 2026.

This article maps what a Visa deposit actually does on the way to your bookmaker's wallet, what triggers a decline, and what the 1 October 2026 surcharging reform from the Reserve Bank does to the cost stack underneath every Visa Debit deposit you make. The numbers come from ACMA quarterly reports, AUSTRAC rulings, the RBA's Payment Systems Board conclusions paper, and H2 Gambling Capital's offshore-market analysis. Nothing in here is a "best site" recommendation, and you will not find a top-five table of operators dressed up as analysis.

The State of Visa Betting in Australia, in 90 Seconds

- Visa Credit cards have been banned for licensed Australian online wagering since 11 June 2024, with operators facing penalties up to AU$247,500 per breach.

- Visa Debit remains the workhorse card rail. Deposits are instant, withdrawals via Visa Direct usually clear in two to five business days.

- Since 29 September 2024, your full ACIP identity check must complete before any deposit settles, and from 2026 the AUSTRAC verification trigger drops from AU$10,000 to AU$5,000 a day.

- The RBA's Payment Systems Board has confirmed surcharging on Visa, Mastercard and eftpos ends on 1 October 2026, which reshapes how bookmakers price and pass through card costs.

- PayID over the New Payments Platform is now the most realistic alternative to Visa, and one major operator has already retired direct bank transfer in its favour.

What Changed on 11 June 2024

I remember the week before 11 June 2024 like a weather front rolling in. Operators had been quietly reconfiguring payment pages for months, but the inboxes I monitored still filled up with confused punters trying to top up with their Mastercard credit card the night before kickoff. By Tuesday morning, the rail was gone for good.

The legal trigger was the Interactive Gambling Amendment (Credit and Other Measures) Act 2023, which took effect on 11 June 2024. From that date, online and phone wagering services may not accept payments funded by a credit card, by a credit-related product, or by a digital currency. The ban is enforceable by ACMA with a maximum civil penalty of AU$247,500 per breach for the operator. There is no equivalent fine on the punter, but no operator in the country will quietly let you slide a credit card past their cashier either.

What "credit-related product" actually covers

The phrase reaches further than a plain Visa or Mastercard credit card. It captures buy-now-pay-later facilities, credit-funded prepaid cards, and digital wallets where the underlying funding instrument is a credit line. If an Apple Pay token resolves to a Visa credit card, the operator must decline the deposit the same way they would decline the physical card. The detail lives in the cluster on the 2024 credit-card ban explained end-to-end.

Why did Canberra do it? The Minister for Communications, Michelle Rowland, framed it bluntly: "Australians should not be gambling with money they do not have. Last year, the Albanese Labor Government committed to banning credit cards for online wagering — and we've delivered." Her colleague Amanda Rishworth added the symmetry argument the political coalition had been building for years — you cannot use a credit card to bet at a TAB shop or a casino floor, so why should the online channel be different.

The industry's lead body, Responsible Wagering Australia, lined up behind the change. RWA chief Kai Cantwell called it "an important measure to protect customers, making it easier for people to stay in control of their own gambling behaviour", which from a peak body that represents the largest licensed bookmakers in the country is as warm an endorsement as a regulator ever gets.

The compliance work that followed was enormous. ACMA's desk-based review in March 2025 found fifty licensed operators still carrying outdated mentions of credit cards or cryptocurrency in their terms and conditions. Every one of them removed those references by 30 June 2025. The same year, Betchoice was hit with a one-million-dollar fine and a mandatory two-year independent review. The rest of the industry watched and updated their internal training accordingly.

The ban includes a built-in feedback loop. The Department of Infrastructure has confirmed the policy will be reviewed two years after commencement, which means the assessment is happening now in 2026. Whatever the review produces, the practical consequence for you as a Visa-using punter is unchanged for the foreseeable future. The credit rail is closed.

The June 2024 credit ban is not a phase. It is a structural shift backed by a fine large enough to keep every licensed operator honest.

The Four Faces of Visa at an Australian Bookmaker

Here is a question I get more than any other: "Mate, my Visa got declined and the bank says nothing's wrong with the card." Nine times out of ten, the answer is that the card in question is actually four different products in a trench coat, and the bookmaker only accepts one of them. Visa is a network, not a single product.

Globally, Visa is the dominant payment card with a 52.8 percent share of all banking cards in circulation and more than 3.3 billion cards in 2026. In Australia, the network rides on top of an AU$1.1 trillion card-payments economy. The catch is that "Visa" on a card face tells you almost nothing about whether the payment will go through.

Visa Credit

The classic charge product. Funds drawn from a revolving credit facility issued by an Australian bank or non-bank lender. Since 11 June 2024, this card cannot fund a deposit at any licensed Australian wagering operator. Bookmakers detect it through the Bank Identification Number, the first six to eight digits of the card. If your Visa card's BIN flags it as credit, the cashier blocks the transaction at the moment of submission, before it reaches your bank.

Visa Debit

The workhorse. Funds drawn directly from your transaction or savings account, with no credit line involved. This is the card type the credit ban left untouched, and it accounts for the bulk of card deposits I see in compliance reviews. A Visa Debit card does not extend credit, does not attract cash-advance fees, and is fully eligible at every licensed Australian operator that lists Visa as a deposit method.

Visa Prepaid

A reloadable or single-load card that holds a balance you have already funded. Bank-issued prepaid Visa cards loaded from your own debit account behave like Visa Debit at a bookmaker. Fintech-issued reloadable prepaid cards sit in a greyer zone — some bookmakers accept them, others reject them outright because the issuer is not on the operator's approved BIN list. Gift Visa cards are almost always rejected, partly because the cardholder name does not match the betting account, partly because anti-money-laundering policy treats them as anonymous.

Co-branded Visa

Cards issued by a financial institution in partnership with a bookmaker brand. Familiar examples are the Sportsbet Cash Card and historical Ladbrokes-branded cards. Most started life as withdrawal-only instruments. Their funding side has been reshaped by the credit ban, and operators have largely retooled them to operate within the debit-only universe.

| Visa product | Funding source | Allowed for AU betting | Typical use |

|---|---|---|---|

| Visa Credit | Revolving credit line | No, banned since 11 June 2024 | Day-to-day spending, travel |

| Visa Debit | Linked transaction account | Yes | Primary betting deposit rail |

| Visa Prepaid (bank-issued) | Pre-loaded balance from debit | Generally yes | Budget control, separate wallet |

| Visa Prepaid (gift) | Pre-loaded by purchaser | Generally no | Retail gifting, blocked at cashier |

| Co-branded bookmaker Visa | Bookmaker-linked balance | Yes, within the issuing brand | Withdrawals, branded ecosystem |

BIN (Bank Identification Number) — the first six to eight digits of a card number, which identify the issuing bank and the product category. Bookmakers maintain blocklists at the BIN level to enforce the credit ban automatically.

The reason the four-way split matters in 2026 is enforcement automation. Bookmakers no longer rely on you to declare what kind of card you are using. The cashier reads the BIN, classifies the card, and either accepts or refuses in milliseconds. For the deeper read on issuer behaviours and what to do when a debit card gets misclassified as credit, see Visa Debit betting sites in Australia.

How a Visa Deposit Actually Reaches a Bookmaker

Punters often picture a Visa deposit as a single transaction. It is not. It is a four-party conversation that starts on your phone, hops to a payment gateway, ricochets through Visa's authorisation network, and lands on your bookmaker's wallet — usually inside three seconds. Knowing where it can break saves an hour on the phone with a call centre.

The first step you do not see is the verification check. Since 29 September 2024, every licensed online wagering provider must complete the AUSTRAC Applicable Customer Identification Procedure before they create the account or provide any designated service. Translation: if your KYC is incomplete, your first deposit cannot settle. The cashier may show a "verification required" banner, or it may simply fail with a generic message. Either way, the card was never the problem. The compliance flag was.

Once your identity is in good standing, a Visa Debit deposit follows this path:

Anatomy of a Visa Debit deposit at an Australian bookmaker

- You enter your card number, expiry, and CVV (or pick a saved card).

- The bookmaker's payment gateway tokenises the card and sends an authorisation request to Visa.

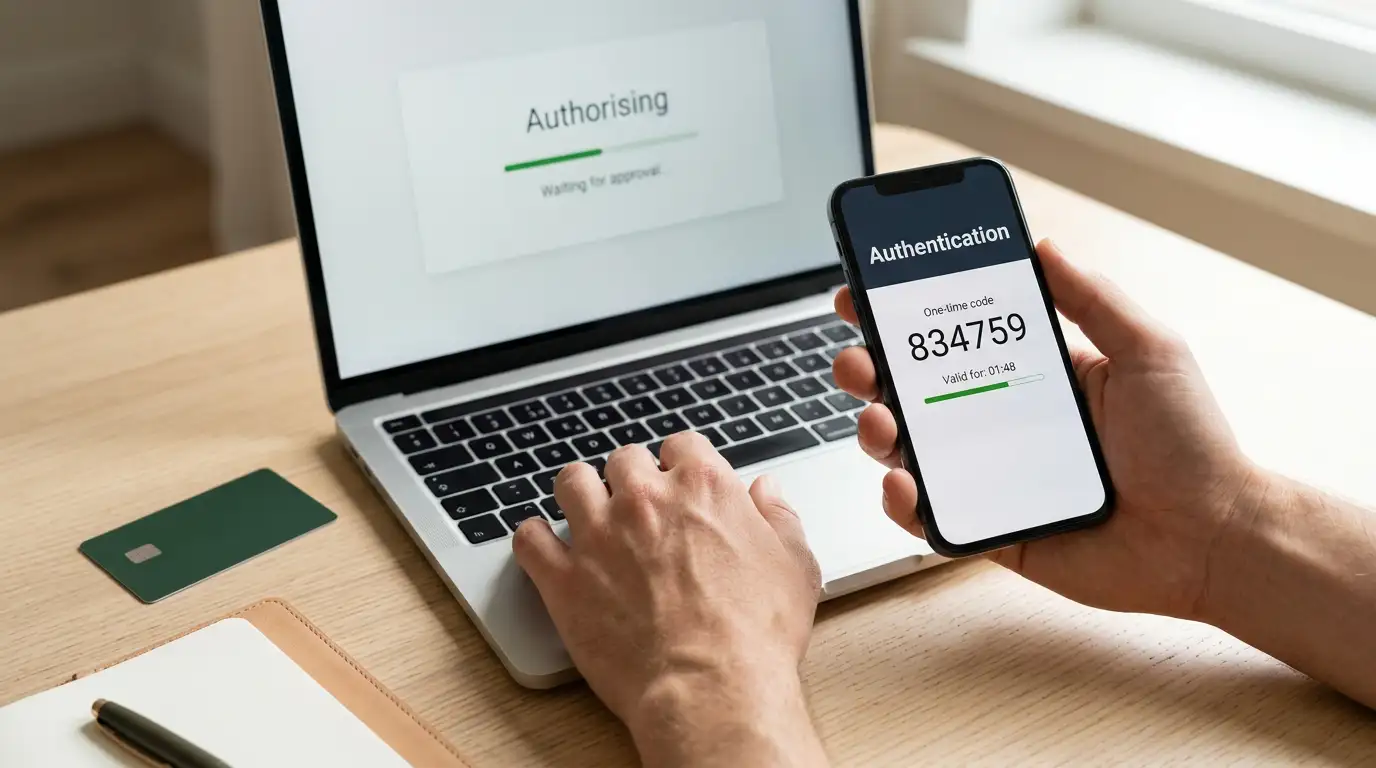

- Visa routes the request to your card issuer, who checks balance, fraud rules, and any active gambling block.

- Your issuer either approves, declines, or triggers a 3D Secure challenge requiring an OTP or app confirmation.

- If approved, funds are reserved and the bookmaker credits your wallet instantly while settlement happens later in the day.

3D Secure — a card-present authentication protocol used online, branded as Verified by Visa. It adds a step where your bank confirms it is really you, often through an OTP sent to your phone or a push notification in the bank's app.

MCC 7995 — the Merchant Category Code that identifies a transaction as a betting or gambling payment. Issuers use MCC 7995 to apply gambling-specific blocks and to flag transactions for compliance monitoring.

The number of moving parts is why deposits sometimes feel slow. The New Payments Platform processes more than 1.4 billion transactions worth over AU$220 billion a year in real-time, but Visa's authorisation network is a separate rail with its own latency. A "delayed" Visa deposit is usually waiting on a 3D Secure step you have not noticed in your banking app.

Two things go wrong more than the rest, and they are unrelated to your bank balance. First, the issuer's gambling switch. Most Australian banks now offer a gambling block that flips your card off for any merchant coded as MCC 7995. Many punters turn it on during a self-imposed cool-down then forget. Second, the operator's velocity rules. If you have made several deposits in a few minutes, the bookmaker's risk engine may force a manual review. Your card is fine. The system is doing its job.

One operational shift worth flagging: from 18 March 2025, Sportsbet stopped accepting direct BSB and account-number transfers and pointed customers towards PayID instead. The change reflects a broader trend — card rails and PayID over the NPP are absorbing what used to be slow, manual bank transfers. The path you choose changes more than just speed — it changes which dispute mechanism you can call on if something goes wrong.

The pre-flight is simple. Confirm your Visa Debit card name matches your betting account name letter for letter. Confirm your KYC is fully verified. Confirm your bank's gambling switch is off. If those three are true and the deposit still fails, the issue is almost always the card type, not the card itself.

Withdrawals via Visa: The Short Version

Withdrawing winnings to a Visa card sounds like running the deposit in reverse. It is not. The deposit is an authorisation. The withdrawal is a push to a card, governed by entirely different scheme rules and a closed-loop convention that bookmakers honour for compliance reasons.

The mechanism behind a card withdrawal is Visa Direct, sometimes called Original Credit Transaction or OCT. Instead of charging the card, the bookmaker tells Visa to push funds to it. The pull-versus-push distinction matters because it determines who controls the timing. With a deposit, your bank can authorise instantly. With Visa Direct, the bookmaker initiates and Visa relays, but funds usually post when your issuer's batch processing settles, which is why the experience feels slow even when the rail itself is fast.

For a Visa Debit cardholder at a major Australian operator, a withdrawal request submitted before lunchtime on a business day typically lands in the account within two to five business days. Some issuers post on the same day. Others wait until the next clearing cycle. Weekends and public holidays add latency on the issuer side, not the bookmaker side.

The closed-loop policy is the rule that says winnings can only be paid back to the same card you deposited from. Operators apply it because it is the cleanest defence against money-laundering schemes that use a betting account as a turnstile between two unrelated cards. If you deposited via PayID and won, the bookmaker may pay you back to your linked bank account by default, simply because the closed-loop rule travels with the deposit method.

Sensible withdrawal habits

- Use the same Visa Debit card for both deposit and withdrawal where possible.

- Keep your card details current — an expired card forces a slower bank-transfer fallback.

- Submit withdrawals during business hours so the issuer's clearing posts the same week.

Habits that delay your money

- Requesting a withdrawal to a card you have not deposited from in twelve months.

- Mixing rails — depositing via PayID and expecting Visa-speed payout.

- Triggering AUSTRAC verification with a large request before your KYC tier is upgraded.

One detail to keep in your head: a Visa Direct credit usually appears on your bank statement as a credit line item separate from any merchant deposit history. The descriptor varies by issuer, but it almost never says "betting" in plain English. That can confuse first-time withdrawers scrolling for a familiar name.

For the granular withdrawal mechanics — closed-loop nuances, issuer-by-issuer posting times, AUSTRAC's role on large payouts, and what happens when an operator forces a bank transfer instead — head to Visa withdrawals from Australian bookmakers.

The Three Regulators Watching Every Card Transaction

If you have ever wondered why a Visa deposit at an Australian bookmaker feels more bureaucratic than the same card paying for groceries, the answer is that three regulators are watching the transaction at the same time. Each has its own remit and its own enforcement appetite. Once you understand who does what, the friction makes sense.

ACMA — the conduct regulator

The Australian Communications and Media Authority enforces the Interactive Gambling Act 2001, including the credit-card ban. ACMA does not licence operators (state and territory regulators do that), but it polices conduct across the federation. In the second quarter of 2024 alone, ACMA received 514 complaints and inquiries, of which 463 — roughly 90 percent — were valid for investigation under the IGA. Across 2024 and 2025, ten new investigations were opened and ten closed, with the Betchoice fine of one million dollars being the standout enforcement outcome.

ACMA's footprint extends beyond fines. The eight-year run of expanded enforcement powers has driven roughly 220 unlicensed operators out of the Australian market entirely. Their March 2025 desk review of fifty licensed operators that still mentioned credit cards or cryptocurrency in their terms ended cleanly: every one of those references was removed by 30 June 2025.

ACMA chair Nerida O'Loughlin on the offshore risk:

Speaking about unlicensed offshore sites, the ACMA chair has put it bluntly: "If one of these sites decides to keep your money, and we know that happens quite regularly, there is nothing you can do about it." Visa chargebacks against offshore operators rarely succeed, and there is no Australian regulator with jurisdiction to recover funds for you.

AUSTRAC — the financial-crime regulator

The Australian Transaction Reports and Analysis Centre runs the anti-money-laundering and counter-terrorism-financing regime. From 29 September 2024, every online gambling provider must conduct their full ACIP — the Applicable Customer Identification Procedure — before creating a customer account or providing any designated service. There is no longer a window where you can deposit and verify later.

ACIP — the AUSTRAC-mandated customer identification procedure required of all designated services. For wagering operators it includes verifying full name, date of birth, and residential address against an independent source.

The other AUSTRAC change worth marking on your calendar is the threshold for wagering operators. From 2026, the trigger for mandatory enhanced verification dropped from AU$10,000 to AU$5,000 a day under the AML/CTF Amendment Act 2024. If your daily Visa deposits cross AU$5,000, expect a verification request beyond the standard ACIP set, even if your account has been in good standing for years.

RBA — the payments-system regulator

The Reserve Bank of Australia, through its Payments System Board, sets the rules for how cards, surcharges and interchange fees behave across every merchant in the country. The headline change is the conclusions paper finalised in March 2026, which confirmed the end of surcharging on eftpos, Mastercard and Visa from 1 October 2026. I cover the implications later in this guide.

The three regulators do not co-ordinate moment to moment, but they share information when patterns emerge. A Visa deposit that triggers an AUSTRAC suspicious-matter report can also surface in an ACMA conduct review if the bookmaker is under audit.

Visa Debit Versus PayID at a Glance

A reader once put it to me this way: "I've got both. Why pick?" Fair question. Visa Debit and PayID solve overlapping problems with different mechanics, and the right answer depends on what you optimise for.

PayID rides the New Payments Platform, the real-time clearing system that processed more than 1.4 billion transactions worth over AU$220 billion in 2023. The rail is fast, free at the consumer level, and uses an alias — your phone number, email, or ABN — instead of exposing your BSB and account number. Visa Debit, by contrast, runs on the four-party card model and carries scheme fees and interchange that the bookmaker pays, even when you do not see a surcharge.

| Dimension | Visa Debit | PayID |

|---|---|---|

| Deposit speed | Instant authorisation | Real-time settlement on NPP |

| Withdrawal speed | 2 to 5 business days via Visa Direct | Often within minutes when supported |

| Cost to bookmaker | Interchange and scheme fees | Lower — flat NPP processing |

| Cost to punter | None directly, surcharge ends Oct 2026 | None |

| Fraud protection | Card-scheme chargeback rights | Bank-side dispute, no scheme protection |

| Identity exposure | Card number, name, expiry | Alias only, BSB stays hidden |

| Closed-loop on payouts | Yes, return to deposit card | Yes, return to PayID alias |

The pragmatic take I give most punters: Visa Debit gives you scheme-level dispute rights that PayID cannot match. If a deposit is duplicated, if a withdrawal goes missing, if a fraud transaction shows up on your card, the chargeback machinery is heavier and more punter-friendly on the card side. PayID is faster and cheaper at scale, but the dispute process leans on bank goodwill rather than scheme rules.

Operator availability matters too. Sportsbet's retirement of direct bank transfer in March 2025 reflects how the industry is consolidating around two rails: a card rail and a PayID rail. If you have a single bookmaker preference, check which rails they pay out on before picking your deposit method, because the deposit rail influences the withdrawal default.

For the side-by-side analysis with the actual numbers, the dedicated comparison sits at Visa versus PayID for Australian betting deposits.

Where Card Rails Meet Responsible Gambling Tools

The first time I sat across from a bookmaker compliance lead and asked how the National Self-Exclusion Register interacts with their Visa cashier, the answer was immediate: "It's the first check we run, before we even look at the card." The payment rail is downstream of the responsible-gambling check, not parallel to it.

BetStop, the National Self-Exclusion Register, has been quietly absorbing a significant slice of the Australian betting population. By the end of the first quarter of the 2025 to 2026 financial year on 30 September 2025, 49,382 people had registered with BetStop, of whom 31,838 held active exclusions. The same quarter saw 4,541 new registrations. By the end of June 2025, 30,032 active exclusions were in place and 14,809 people had either completed their exclusion period or ended it early.

Roughly half of Australians who gamble offshore are simultaneously registered on BetStop. The system catches the licensed channel cleanly, but the offshore back door defeats it for users who actively look for it.

If you are on BetStop, your Visa card is functionally inert at every licensed Australian wagering operator. The cashier will not let the deposit reach Visa's authorisation network. ACMA chair Nerida O'Loughlin has framed the register's value this way: "Online gambling can cause a great deal of harm to individuals, their families and friends, so it's encouraging that so many people have decided to take the step and register to self-exclude. Younger Australians in particular are making early decisions about the role that online gambling will play in their lives."

The bookmaker's cashier checks your account against the register before any payment screen appears. If you are excluded, the deposit form is hidden entirely. If you registered after a deposit was already in flight, the operator must refund and close the account. The card-side blocking offered by major banks is independent and additional — your bank can refuse Visa transactions to gambling merchants even if the bookmaker is willing to process them.

The card itself plays a role in harm-prevention beyond the regulator's framework. About 46 percent of those who gamble in Australia have been classified as at risk of harm, which is a sobering number to hold in your head when you are setting deposit limits in a betting app. The deposit-limit tool is mandatory under the National Consumer Protection Framework. Setting one is the difference between a discipline that holds and a Saturday night that doesn't.

The Numbers Behind the Australian Wagering Market

Step back from the Visa cashier and look at the country's gambling balance sheet. The numbers are jarring in a way that puts the regulator's caution into context, and they explain why the credit ban arrived when it did. Visa is one rail through a market that moves more money than any equivalent population in the world.

AU$32 billion

Total Australian gambling losses in 2024 — the largest annual loss ever recorded.

AU$244.3 billion

Total amount staked in 2022 to 2023, making Australia the world's leading gambler per capita.

USD 5.5 billion

Australian online gambling market value in 2025, projected to reach USD 9 billion by 2034.

AU$3.9 billion

Volume of unlicensed offshore wagering in Australia in 2024 — and rising.

Australians lost AU$31.5 billion in the 2022 to 2023 financial year, with the average per-capita loss landing at AU$1,527. The 2024 figure, AU$32 billion, set a fresh ceiling. Tim Costello of the Alliance for Gambling Reform has summed up the trajectory in plainer terms: "Online betting has spiked by more than 50% in the last five years with losses now totalling $9 billion dollars, undermining Prime Minister Albanese's comments that online gambling isn't the problem."

Participation is broad rather than concentrated. Some 73 percent of Australians aged eighteen and over participated in at least one form of gambling within a twelve-month window, and 38 percent gamble at least weekly. Sports betting specifically reaches 33.8 percent of Australian adults inside any twelve-month period.

Around 80 percent of all Australian bets are placed on a mobile device. Your Visa Debit card is a phone screen away from a bookmaker's cashier, every minute of the day.

The offshore picture is the uncomfortable counterweight. Some 36 percent of all online betting in Australia now flows through offshore services — up from 26 percent in 2021, on H2 Gambling Capital's reading of the offshore market for Responsible Wagering Australia. One in every five dollars spent on sports betting in Australia goes through an unlicensed operator. About a third of offshore gamblers used credit funds despite the June 2024 ban on the licensed channel.

Why does this matter for your Visa card? Every consumer protection — the credit ban, ACIP, BetStop, deposit limits, AUSTRAC oversight — is enforceable on a domestic operator and unenforceable on a Curacao-licensed sportsbook. About 6 percent of Australian adults report being harmed by someone else's gambling. The licensed industry serves around ninety online bookmakers under Australian licences, with 134 active services counted in April 2026. Kai Cantwell, who runs Responsible Wagering Australia, put the trade-off plainly: "Australia's world-leading consumer protections are only effective if people stay within the system, and right now, it's too easy to bypass them offshore with a few clicks."

The 1 October 2026 RBA Reform and What It Means for Visa Punters

If you remember one date from this guide other than 11 June 2024, make it 1 October 2026. That is the day Australia stops allowing surcharging on eftpos, Mastercard and Visa transactions — credit, debit and prepaid alike — at every merchant in the country, including bookmakers. The reform was finalised by the Reserve Bank's Payments System Board in March 2026.

The PSB framed it in the conclusions paper this way: "Removing surcharging would make card payments simpler, more transparent and help to increase competition in the card payments system. Around 90 per cent of Australian businesses are estimated to be better off under the proposed policies." Australian consumers currently pay roughly AU$1.2 billion a year in card surcharges, and the RBA's view is that the surcharging regime stopped serving its original purpose once card costs themselves came down.

What the reform actually changes

Two pieces matter for Visa betting deposits. First, the surcharging ban removes the merchant's right to add a separate fee on top of a card transaction. Second, the RBA is also tightening interchange caps — the wholesale fees the issuer charges the acquirer — which lowers the cost of accepting a Visa Debit card in the first place.

For most punters at most licensed Australian bookmakers, the surcharge change is more philosophical than practical. Major operators have not been surcharging Visa Debit deposits anyway — they absorb the cost as part of customer acquisition. Where the reform bites is at smaller bookmakers and specific deposit pathways where a "service fee" was being applied. After 1 October 2026, those fees vanish.

The interchange angle is more strategically interesting. Card payments in Australia hit AU$1.1 trillion in 2025 with a 10.3 percent compound annual growth rate over 2021 to 2025. If interchange caps come down and surcharging cannot recover the cost on the merchant side, the card economics for bookmakers tilt slightly more favourably. Whether that translates into faster Visa Direct payouts, looser deposit limits, or simply better margins depends on each bookmaker's commercial choices.

One subtle effect to watch: PayID's relative cost advantage compresses. Today, the cost gap between a card deposit and a PayID deposit is the main reason some operators nudge customers towards PayID at the cashier. If interchange falls and surcharges disappear, the nudge weakens. Visa Debit becomes a more level competitor on the cost stack.

The reform applies to all eftpos, Mastercard and Visa cards used at Australian merchants, regardless of where the card was issued. International Visa cards used at Australian bookmakers benefit from the same no-surcharge rule, although foreign-transaction fees set by the issuer's home market remain unaffected.

The Quick Map of Why a Visa Deposit Gets Refused

Picture this scene. You are at the pub on grand-final day, twenty minutes to first whistle, and your Visa Debit just got knocked back at the cashier. The barman is patient. The friend group is not. Here is the diagnostic order I run, ranked from most common to least, before anyone phones a bank.

Check first

- Card type — is it Debit, not Credit?

- Bank gambling switch — is it off in your banking app?

- 3D Secure — did you respond to the OTP or app prompt?

- KYC status — has your ACIP fully cleared?

- Card name match — does the card holder match the betting account exactly?

Common dead ends

- Assuming the bookmaker has the wrong information.

- Repeatedly retrying — issuer fraud rules tighten with each attempt.

- Switching to a credit card "just to test" — guaranteed decline.

- Calling the bookmaker before the bank.

The most common cause in 2026 is the credit-versus-debit detection at the BIN level. Many punters carry a Visa product that looks like debit on the card face but is technically a credit instrument under scheme rules. Charge cards, certain neobank cards funded by an overdraft, and some travel-money cards fall into this trap. The bookmaker reads the BIN, classifies the card as credit, and refuses cleanly. Your bank shows nothing wrong because the transaction never reached them.

The second most common is the issuer-side gambling block. Most major Australian banks now offer a self-imposed gambling switch in their app. The block applies to MCC 7995 — the merchant category code for betting and gambling — and operates independently of the bookmaker. If the switch is on, every deposit fails until you turn it off, with most banks adding a 24 to 72 hour cooling-off period before the change takes effect.

SCA (Strong Customer Authentication) — the regulatory term for two-factor authentication on payment transactions. Many issuers now apply SCA-style challenges to gambling deposits as a matter of course.

Failed 3D Secure challenges are the third bracket. The OTP arrives, you do not enter it in time, the transaction times out. The fix is usually to wait fifteen minutes and try again with the OTP open ready. If the issue repeats across several deposits, your bank's fraud rules may have flagged your account, and a phone call to the fraud line clears it.

Incomplete ACIP is the fourth and most overlooked. If your account was created after 29 September 2024, no deposit can settle until your full identity verification has cleared. The fix is patience and a clean re-upload of identity documents.

The full decision tree, with each cause broken into sub-causes and fixes, lives at why your Visa deposit gets declined at an Australian bookmaker. If you are reading this from the pub on grand-final day, the short version: try a Visa Debit you have used before, check your bank app for an active block, and if both fail, switch to PayID for the night and sort the card out tomorrow.

The Australian Bookmaker Landscape Through a Visa Lens

One stat I keep on a sticky note above my monitor: 134 active online wagering services were operating under Australian licences in April 2026, sitting on top of an underlying licensed bookmaker count somewhere north of ninety. The market is large, fragmented, and not as homogeneous as the headline players make it look.

How licensed Australian bookmakers fall into Visa-relevant groups

The market splits into roughly three tiers when you look at it through a payments lens: tier-one corporate operators with full Visa Debit, Visa Direct payouts, PayID, and bank transfer; tier-two operators with Visa Debit and PayID but not always full Visa Direct support; and a long tail of niche operators where Visa Debit is offered but withdrawal pathways skew towards bank transfer or PayID only.

The headline difference between tiers is on the withdrawal side. Tier-one operators usually support Visa Direct payouts as a default, which is how a punter with a recently-used Visa Debit card gets winnings inside the two-to-five business day window. Smaller operators may push every withdrawal through bank transfer because the operational cost of integrating Visa Direct is non-trivial relative to their volume. That is not a quality signal — it is a scale signal — but it changes your experience of the same Visa card across operators.

The deposit experience is more uniform than the withdrawal experience. Visa Debit acceptance is now near-universal at licensed Australian operators. Where you see variation is in card-on-file behaviour, 3D Secure cadence, and the deposit limits applied by default to new accounts. None of that is reflected in advertising. All of it is reflected in your day-to-day experience.

The retirement of direct bank transfer at Sportsbet from 18 March 2025 was a leading indicator of where the industry is going. The bookmaker pointed customers explicitly at PayID as the replacement, signalling that the future cashier has two prominent rails — a card rail and PayID — with bank transfer treated as legacy infrastructure.

The licensed bookmaker count has been remarkably stable for several years even as offshore activity has grown. Every market exit ACMA documents is offset by a new entrant under a state or territory licence.

What I do not do — and what you will see plenty of other sites do — is rank operators by their Visa handling. The reason is structural. Acceptance is largely uniform, and the differences that do exist shift quarterly as operators tune their compliance and risk engines. A "best Visa bookmaker" list dated this month is half-wrong by next quarter. The honest read is: pick a licensed operator on grounds that matter to you (product range, bonus structure, customer service), then validate that their Visa rail behaves the way you need it to.

Frequently Asked Questions About Visa Betting in Australia

The questions in this section are the seven I get asked most often by Australian punters on the phone, in compliance reviews, and in DMs from readers. I have kept the answers short. Each links into a dedicated cluster where deeper detail lives.

Can I use a Visa credit card to bet online in Australia?

No. From 11 June 2024, every licensed Australian wagering operator is prohibited from accepting deposits funded by a credit card or any credit-related product, including credit-funded digital wallets. The penalty for an operator breach is up to AU$247,500. Visa Debit remains fully eligible.

Are Visa deposits to Australian bookmakers instant?

Yes for deposits, no for withdrawals. A Visa Debit deposit clears authorisation in seconds and your betting wallet is credited immediately. A Visa Direct withdrawal usually takes two to five business days to post to your bank account, depending on the issuer's clearing schedule.

Are there fees for using Visa at Australian betting sites?

Major licensed bookmakers do not charge a deposit fee on Visa Debit. The cost stack — interchange and scheme fees — sits with the bookmaker. From 1 October 2026, surcharging on Visa is banned at every Australian merchant, so the surcharge route closes for any operator who was using it.

Why was my Visa declined when depositing at a bookmaker?

The four most common causes, in order: the card is technically a credit product under the BIN, your bank's gambling switch is on, a 3D Secure challenge timed out, or your ACIP identity verification has not fully cleared. The full diagnostic tree lives in the dedicated cluster on declines.

Can I withdraw winnings back to my Visa card?

Most tier-one Australian operators support Visa Direct payouts to the same Visa Debit card you deposited with — the closed-loop policy. Smaller operators sometimes route withdrawals through bank transfer instead. If you deposited via PayID, the operator may pay you back to your linked bank account by default rather than to a Visa card on file.

What are the safer alternatives to Visa for Australian betting deposits?

PayID over the New Payments Platform is the leading alternative — instant, free, and your BSB stays hidden. POLi, Apple Pay or Google Pay (when funded by a debit card), bank transfer at smaller operators, and bank-issued prepaid Visa cards are also available. Each has trade-offs around speed, dispute rights, and bookmaker support.

How does the Reserve Bank's 2026 surcharging reform affect Visa betting deposits?

From 1 October 2026, no Australian merchant — bookmakers included — can add a surcharge to a Visa, Mastercard or eftpos transaction. The RBA is also tightening interchange caps. The combined effect lowers the operator's cost of accepting Visa Debit, which may translate into faster Visa Direct payouts or relaxed deposit defaults at some operators over time.

The Analyst's Last Word for the Australian Punter

Eleven years in this corner of payments and wagering has taught me to distrust certainty. Rules change. The two-year review of the credit ban is happening now in 2026, and whatever it produces will reshape some answers above. So my closing word is not a prediction. It is a posture.

Use the licensed channel. The card-side architecture in Australia — ACIP pre-verification, BetStop, deposit limits, AUSTRAC oversight, the credit ban — exists because the regulator has built a system that protects punters when things go wrong. H2 Gambling Capital, writing for Responsible Wagering Australia, put the alternative bluntly: "Australia is the only mature betting market not to allow in-play wagering online. Nearly one in five offshore sports betting customers said access to live in-play betting was their primary reason for using illegal sites." The punter who follows that pull loses every consumer protection their Visa card gives them on home soil.

Match the rail to the moment. Visa Debit is the right answer when scheme-level dispute rights matter and when your operator pays out via Visa Direct. PayID is the right answer when speed and cost trump those benefits. Treat the choice as a tool selection, not a brand loyalty.

And keep one eye on the calendar. The June 2024 credit ban set the floor. The September 2024 ACIP rule reset account-opening. The 2026 AUSTRAC threshold drop tightened the enhanced-verification trigger. The October 2026 surcharging reform takes the last obvious cost lever off the table.

The right Visa card and the right rail will not change your luck on a Saturday night, but they will protect your money on a Sunday morning. The licensed channel, the matching debit instrument, the correct KYC tier, and the awareness of when each regulator's rule applies — that is the ledger that pays out.