Daily Visa Deposit Limits Explained

The cap that exists three times over

One of the more confusing facts of Australian betting in 2026 is that there isn’t a single deposit limit on your Visa Debit transactions – there are at least three, and they don’t always align. There’s the limit you set yourself at the bookmaker. There’s the operator’s own cap, which they apply across all customers regardless of individual settings. And there’s the National Consumer Protection Framework that sits over the top of both, with its own logic about voluntary versus involuntary controls.

The problem isn’t that the system has too many limits – it’s that the customer doesn’t always know which one stopped their deposit. A failed AU$2,000 deposit could be your own limit kicking in, the operator’s transaction cap, or an NCPF flag triggering on velocity. The fix for each is different, and treating one as another wastes time and patience. So this piece pulls them apart.

I’ll walk through what the National Consumer Protection Framework actually does for Visa deposits, where the operator-level caps sit, and how customer-set limits interact with both. The goal is to give you a clean mental model of why your deposit failed and which lever actually unblocks it.

Play responsibly via our homepage.

What the NCPF deposit-limit framework requires

The National Consumer Protection Framework for Online Wagering came into effect in stages from 2018 onwards, with the deposit-limit component requiring all licensed Australian operators to offer customers the ability to set voluntary deposit limits, and to default to a “no preset limit” until the customer makes a choice. The framework was tightened over subsequent revisions, and by 2026 the deposit-limit features at every Australian licensee are essentially uniform: customers can set daily, weekly, monthly, or open-ended limits, the limits apply across all deposit methods (Visa, PayID, others), and the operator must show the customer the limit and any movement against it during the deposit flow.

The voluntary-but-prompted nature of the limits is the framework’s signature design choice. The operator has to actively prompt customers to set limits at signup and at periodic intervals afterwards, but the customer doesn’t have to set one if they don’t want to. This is different from some overseas frameworks where mandatory minimum limits apply.

“This is an important measure to protect customers, making it easier for people to stay in control of their own gambling behaviour,” is how the industry’s peak body framed the deposit-limit rules. The framing matters because it captures the policy intent – voluntary control by customers, with operator-level infrastructure to make those controls work without friction at the deposit screen.

Operator-level caps and how they differ from customer-set ones

Underneath the NCPF customer-facing limits, operators run their own internal caps. The most common operator-level limit is a single-transaction maximum on Visa Debit deposits – typically AU$5,000, AU$10,000, or AU$25,000 depending on the operator’s risk appetite and customer-relationship history. These caps exist to manage the operator’s own exposure to chargebacks and fraud, and they apply regardless of what limits the customer has set.

The interaction can be confusing. A customer with no daily deposit limit set at the operator might still hit the operator’s per-transaction cap of AU$5,000 on a single attempt. The customer thinks “I haven’t set a limit, why is this failing?” when the answer is that the operator’s cap is doing the blocking. The fix is to split the deposit into multiple transactions or use a different rail with a higher transaction ceiling.

The card-payment economy in Australia is enormous – AU$1.1 trillion in 2025, with Visa as the dominant scheme – so operators see plenty of deposit traffic at all sizes. But the per-transaction cap mechanics aren’t going anywhere; they’re a structural part of how operators manage their card-rail risk. The 2024-25 ACMA enforcement work, including the AU$1 million Betchoice fine plus a mandatory two-year independent review, has reinforced operators’ incentives to keep their caps conservative rather than letting them drift upward.

The 2024 AML threshold and its interaction with deposit limits

The Anti-Money Laundering and Counter-Terrorism Financing Amendment Act 2024 dropped the daily KYC threshold for wagering services from AU$10,000 to AU$5,000 effective in 2026. This isn’t a deposit limit per se – it’s an enhanced-procedure threshold – but its practical effect on customers is similar to a soft daily cap.

What happens when you cross AU$5,000 of daily deposit volume at an operator is that the system flags you for additional verification. The flag doesn’t automatically reject your next deposit, but it usually triggers a hold-and-review process where the operator’s compliance team confirms the source of funds and any other AUSTRAC-mandated checks before allowing further deposits to clear. Most cases resolve within a day; some take longer.

For high-volume punters, the 2024 amendment has changed deposit-day planning significantly. What used to be a clear AU$10,000-a-day path is now a AU$5,000 path with a friction wall above it. Punters who occasionally need to deposit larger amounts have adapted by spreading deposits across multiple operators, by using PayID rails (which trigger the same threshold but interact with different caps), or by accepting the friction and working through the enhanced-procedure flow when they need to.

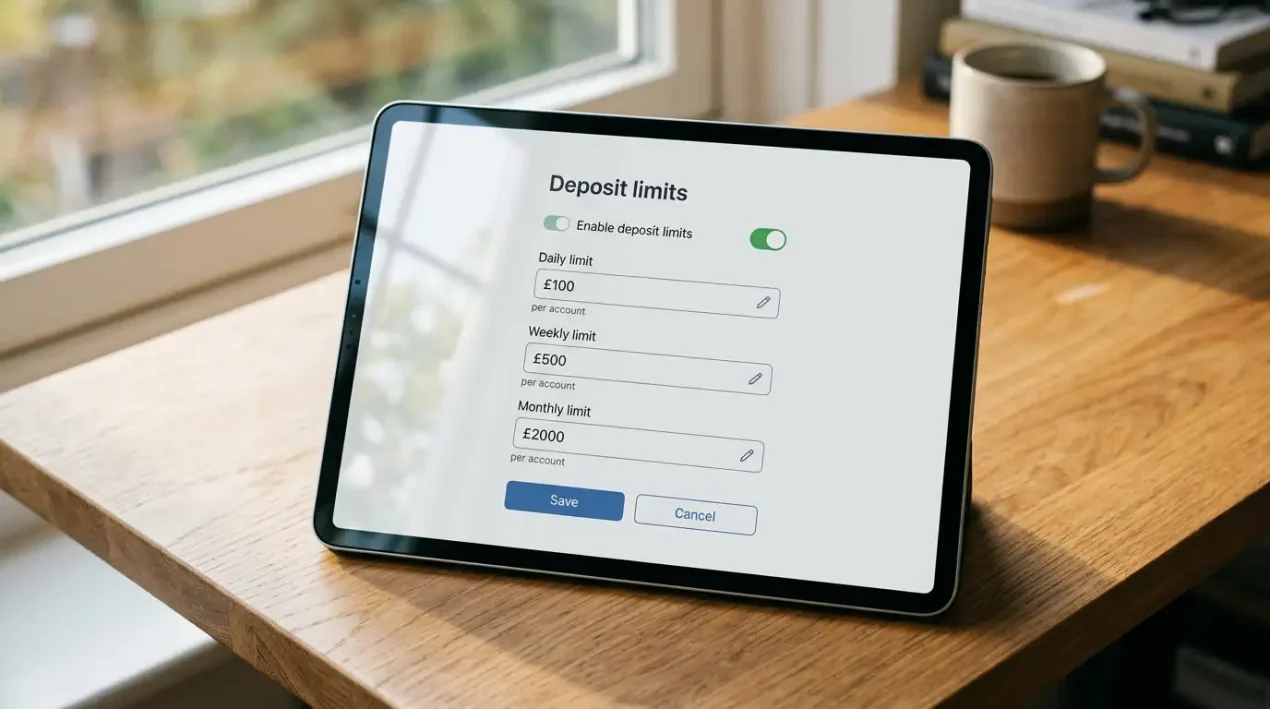

Per-day, per-week, per-month – how customer settings interact

Customer-set limits can stack across timeframes. A punter might have a daily limit of AU$200, a weekly limit of AU$1,000, and a monthly limit of AU$3,000. Each limit applies to its own window, and the strictest one in any given context controls. So in the example, a punter who’s deposited AU$200 today and AU$800 this week can’t deposit any more today (daily limit hit), but can deposit on subsequent days up to the weekly cap, and so on.

Increasing a limit triggers a cooling-off period. The framework requires that any upward limit change has a minimum waiting period – typically 7 days – before the new limit takes effect. Decreasing a limit takes effect immediately. This asymmetric treatment is deliberate; it makes it harder to react impulsively to a losing session by raising your own limit on the spot.

The cooling-off mechanic is one of the more meaningful protections in the framework. A punter who’s lost AU$500 on a bad weekend and wants to chase the loss by raising their daily limit can’t do it instantly – they have to wait a week, by which time the impulse has usually passed. The friction is small but it’s targeted exactly at the behavioural pattern that produces the worst outcomes.

Bookmaker enforcement and the 30-day blocks

Beyond the deposit-limit framework, operators offer voluntary blocks of various durations. The most common are 30-day blocks (you can’t deposit at this operator for 30 days), longer time-outs (90 days, 6 months, a year), and indefinite self-exclusions. These sit above deposit limits – they’re not caps on the rate of deposit, they’re outright denials of access for the specified period.

The headline self-exclusion product is BetStop, the National Self-Exclusion Register. By the end of Q1 of the 2025-26 financial year, BetStop had 49,382 total registrations with 31,838 currently active exclusions, and 4,541 new registrations had come in during that quarter alone. BetStop excludes you from all licensed Australian operators at once, with minimum exclusion periods of 3 months and the option of permanent exclusion.

The interaction with deposit limits is that BetStop overrides everything. While you’re on BetStop, no operator can accept deposits from you regardless of any limits you’ve previously set. When your BetStop period ends and you choose to return, your previous deposit limits at individual operators are still in effect – they don’t reset. The structural protections compound, which is intentional.

What to do when a limit blocks an unexpected deposit

If a deposit fails and you suspect a limit is the cause, the diagnosis is usually quick. Check your customer-set limits at the operator first – they’re the most common cause and the easiest to spot. Then check the operator’s per-transaction cap (usually displayed somewhere in the deposit-method help). Then consider whether you’ve crossed the AU$5,000 AUSTRAC threshold today.

If the issue is your own customer-set limit, the answer is to wait for the period to roll over (next day, next week, next month depending on which limit you hit) or to reduce the deposit size. Increasing your own limit immediately doesn’t work because of the cooling-off requirement.

Learn more about betting taxes in Australia.

If the issue is the operator’s per-transaction cap, split the deposit across multiple transactions or use PayID, which usually has higher per-transaction limits than card rails. If the issue is the AUSTRAC threshold, work through the enhanced-procedure flow rather than trying to bypass it.

For the deeper picture of how the AUSTRAC threshold itself works in practice, my piece on the AUSTRAC AU$5,000 daily threshold for Visa bettors covers the threshold mechanics in detail.

Why was my AU$1,000 deposit declined when my limit is set higher?

The most common reasons are an operator-level per-transaction cap that sits below your customer limit, an outstanding flag from a recent AUSTRAC threshold crossing, or your bank’s own daily transfer limit. Customer-set limits at the bookmaker aren’t the only ceiling on a deposit, and the failure message often doesn’t tell you which ceiling is in effect.

If I increase my daily limit, when does the new limit take effect?

At least 7 days after the change is requested, due to the cooling-off requirement built into the framework. The change isn’t instant. Decreases to limits are immediate, but increases are deliberately slowed to prevent impulse-driven adjustments after losing sessions.

Do limits set at one operator carry across to other AU bookmakers?

No. Customer-set limits are per-operator. You can have AU$200 daily at one bookmaker and AU$5,000 daily at another. The cross-operator equivalent is BetStop, which excludes you from all licensed Australian operators at once. The fragmented nature of per-operator limits is one reason BetStop exists as a complementary mechanism.