MCC 7995: Gambling Merchant Code Explained

The four digits that decide whether your bet goes through

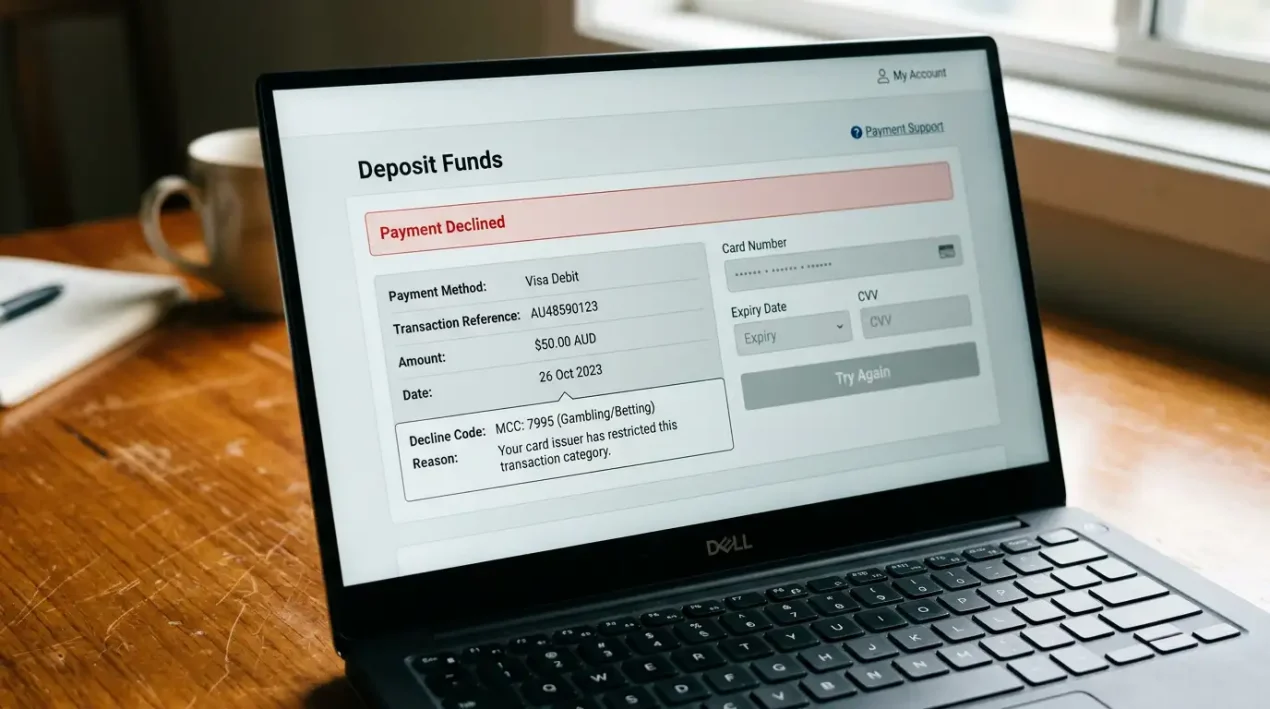

About a year into the credit-card ban, I started keeping a tally of decline reasons that landed in my inbox. By the end of three months I had sixty-eight messages, and forty-three of them traced back to the same four digits: 7995. People were furious because the bank statement said nothing useful and the bookmaker said even less. Both ends of the rail were pointing at each other while the punter sat in the middle wondering whether their card was broken.

It’s not broken. MCC 7995 is doing exactly what it was built to do. The trouble is that almost nobody outside of payments compliance teams has ever heard of it, which means the average bettor is flying blind when their Visa Debit gets bounced from a perfectly legitimate Australian wagering site. This piece pulls the code out into the open and walks through what it actually controls – because once you understand how issuers read those four digits, you stop guessing about declines and start fixing them.

Troubleshoot payments on our website.

What MCC 7995 actually is and where it came from

Merchant category codes are a tagging system that the card schemes – Visa, Mastercard, eftpos and the rest – use to classify what a business sells. Every merchant that accepts cards gets exactly one MCC assigned to them by their acquiring bank, and that code travels with every authorisation request the merchant sends down the wire. A coffee shop is 5814. A petrol station is 5541. A licensed Australian bookmaker is 7995, the same code applied to lotteries, casinos and racetrack betting around the world.

The code matters because it’s the one piece of metadata an issuer can rely on before the transaction settles. It can’t see what you bet on, how much you’ve already deposited this week, or which event the wager covers. It sees the amount, the merchant name, the country, and the MCC. That’s the entire packet. So when a bank wants to make a policy decision about gambling at the moment of authorisation – and most of them now do – the MCC is the lever they pull.

Card payments still dominate the Australian online economy. Card payments value in Australia reached AU$1.1 trillion in 2025 with a compound growth rate above ten per cent over the previous four years, which means the MCC system is sorting through more transactions than ever. Visa and Mastercard between them touch the overwhelming share of those payments. A code that nudges a small fraction of those transactions into a different decision tree ends up shaping the experience for millions of cardholders without any of them noticing – until they try to deposit at a bookmaker and the screen goes red.

How issuers actually use the code

Three banks, three different policies – that’s the shortest honest summary of how Australian issuers handle 7995. One of the big four has had a self-service gambling toggle in its app since well before the credit ban hit, and switching it off doesn’t just block credit-card gambling; it bins every Visa Debit transaction tagged 7995 too. Another runs a softer version where the toggle slows transactions down with extra authentication but doesn’t outright stop them. The smallest of the four leaves the decision largely to the customer’s deposit limits and SCA flow.

What that means in practice is your card might glide through at one bookmaker on a Tuesday night and get bounced at the same bookmaker on Friday morning, even though nothing about your account changed. The bookmaker’s MCC didn’t move. Your balance is fine. What changed is the issuer’s risk model, or your exposure to it – perhaps a velocity check kicked in, perhaps a third deposit in twenty minutes tripped a rule, perhaps your bank quietly tightened its 7995 policy the night before. None of that gets explained in the decline message you actually see, which is usually a bland “transaction not approved”.

The pre-creation verification rules that took effect on 29 September 2024 require all online gambling providers to complete the customer identification procedure before opening an account or providing any designated service. That layer sits on top of the MCC system rather than replacing it, and the two interact in awkward ways. If your bookmaker hasn’t finished pushing your verification through to its banking systems, the issuer might still see a 7995 attempt from a customer it doesn’t recognise as fully onboarded, and that’s a fast path to an automated decline.

Whitelisting versus a hard block

There’s an important distinction most punters never get told about: a hard block and a whitelist are not the same thing, and which one your bank uses determines whether you have any room to manoeuvre at all.

A hard block is a categorical refusal. The bank’s gambling-block flag is on, every 7995 transaction fails, end of conversation. You can’t ask the bank to make an exception for one bookmaker because the rule operates at the category level, not the merchant level. The only way out is to disable the block entirely, wait through whatever cooling-off period the bank imposes – typically forty-eight to seventy-two hours for the major lenders – and then try again, with the block still off.

A whitelist is a different beast. It treats 7995 as a default-deny category but allows specific merchants through if the cardholder requests it. Very few Australian retail banks operate a true whitelist for gambling at the consumer level – most do it only for business accounts where the merchant has applied for an exemption. The neobanks and a couple of the smaller credit unions run something closer to it, where you can flag particular merchants as “trusted” and have transactions to those names treated differently. If your bank offers this, it’s worth knowing because it’s the only path that lets you keep a general gambling block on while still allowing your usual licensed bookmaker to take deposits.

What to actually say when you call your bank

The script that works is shorter than people expect. You don’t need to explain the credit ban, you don’t need to justify your betting, and you definitely don’t need to argue about whether 7995 is fair. Open with: “I’d like to check whether my card has any restriction on merchant category code 7995, and if so what my options are.” That sentence does three things – it tells the rep you know the technical lever, it sidesteps the moral conversation, and it puts the burden on them to look up the actual policy rather than improvise one.

If they confirm a block, the follow-up is: “Can that be lifted on a per-merchant basis, or is it category-wide?” That’s the whitelist question without the jargon. If the answer is category-wide, ask whether they apply a cooling-off period and how long it runs. Get the cooling-off length in writing through the chat or app rather than verbally. I’ve seen people quoted twenty-four hours by phone and then locked out for seventy-two when they tried to deposit.

One thing not to do: never tell the bank you’re calling because a specific bookmaker rejected your card. The decline didn’t come from the bookmaker. The bookmaker forwarded an authorisation request that your bank then refused. Framing it as a bookmaker problem sends the rep down the wrong rabbit hole and adds twenty minutes to the call.

When the decline isn’t actually about MCC

Not every Visa decline at an Australian bookmaker traces back to 7995, and assuming it does will waste your time. Three other patterns produce identical-looking error messages.

The first is BIN-level credit detection. Your bookmaker checks the first six digits of your card against a list of credit BINs and refuses anything that matches before it even hits the network. That’s compliance with the credit ban operating one layer above the MCC system. The second is 3D Secure failure – the OTP that arrives on your phone times out, you mistype the code, or your authenticator app refuses to confirm. The transaction never reaches the issuer’s risk engine, so MCC isn’t relevant. The third is bookmaker-side velocity rules: too many deposit attempts in too short a window, especially after a previous decline, will trigger an internal rate limit that has nothing to do with your bank.

The way to tell which one you’re hitting is the timing and wording of the failure. An MCC block tends to fail fast – within a second or two of clicking deposit – and the message is typically generic. A 3D Secure failure stalls on the authentication screen. A velocity rule shows up as a polite “please try again later” or a cooldown timer. A BIN-level credit refusal often names the card type explicitly: “credit cards are not accepted for wagering deposits in Australia”. If your error matches that wording, MCC isn’t your problem.

The path back from a decline that won’t quit

If you’ve been through the usual fixes and your Visa Debit still won’t deposit, the cleanest move is usually to switch rails for the moment rather than keep escalating with the bank. PayID running over the New Payments Platform settles in seconds, doesn’t rely on MCC at all, and bypasses the card-scheme decision tree entirely. It’s not a perfect substitute – name-match rules at bookmakers can produce their own friction – but it sidesteps the specific problem you’re stuck on.

See our list of Visa sports betting codes for more clarity.

Switching rails also gives you a diagnostic signal. If PayID works and Visa doesn’t, the issue is on the card side, which means your conversation with the bank is still the long-term answer. If PayID fails too, the issue is on the bookmaker side or the verification side, and you need to chase it through the operator’s support team. For the deeper reasons your card might be misclassified by your issuer in the first place, the BIN-range and issuer-code analysis covers what determines how your bank tags individual cards.

Will my bank record an MCC 7995 transaction differently from a regular purchase?

Yes. The transaction sits in the same general ledger as any other card spend, but it’s tagged in your statement metadata as gambling-category. Some banks expose that tag in the app as a separate spending bucket, others surface it only when you export a CSV. Either way the tag is permanent on the record.

Can a merchant disguise the MCC to bypass a block?

No. The MCC is assigned by the merchant’s acquiring bank based on the underlying business activity, not chosen by the merchant itself. A licensed Australian bookmaker that switched its MCC to anything other than 7995 would be in breach of its acquirer’s contract and the card-scheme rules, and would lose its merchant facility. Offshore operators sometimes mis-code, which is one of the warning signs the ACMA flags.

Does a debit card refusal at MCC 7995 affect my credit file?

A declined transaction itself doesn’t generate a credit-file entry. It’s not a missed payment, it’s a non-event from a credit-bureau perspective. Repeated declines might trigger internal monitoring at your bank, but they don’t show up on your Equifax or illion report.