The Cost of Visa Betting Deposits

The cost layers nobody mentions on the deposit screen

When you tap deposit at an Australian bookmaker, your AU$100 lands in your wagering balance and the world looks simple. Between the screen tap and the balance update, though, there’s a full economic stack moving – interchange flowing from the operator’s bank to your bank, scheme fees flowing to Visa, processing fees paid by the operator to its acquirer, and a thin margin retained by the operator after all of that. None of those layers appear on your deposit screen, but they shape what the operator can offer you, what promotions are sustainable, and what the broader Australian wagering economics look like.

The card-payment economy in Australia hit AU$1.1 trillion in value during 2025, and Visa sits on a substantial share of that. Wagering deposits are a small slice, but the fee mechanics at this scale generate real money – both for the operator’s cost stack and for the broader payment-system intermediaries. With the Reserve Bank’s reform package taking effect on 1 October 2026, the cost stack is changing materially, and the punter-facing impact deserves a clearer explanation than it usually gets.

So this piece walks through the actual cost of a Visa betting deposit in Australia: who pays whom, how much, and how the post-October 2026 framework reshapes the picture.

Understand betting costs on our website.

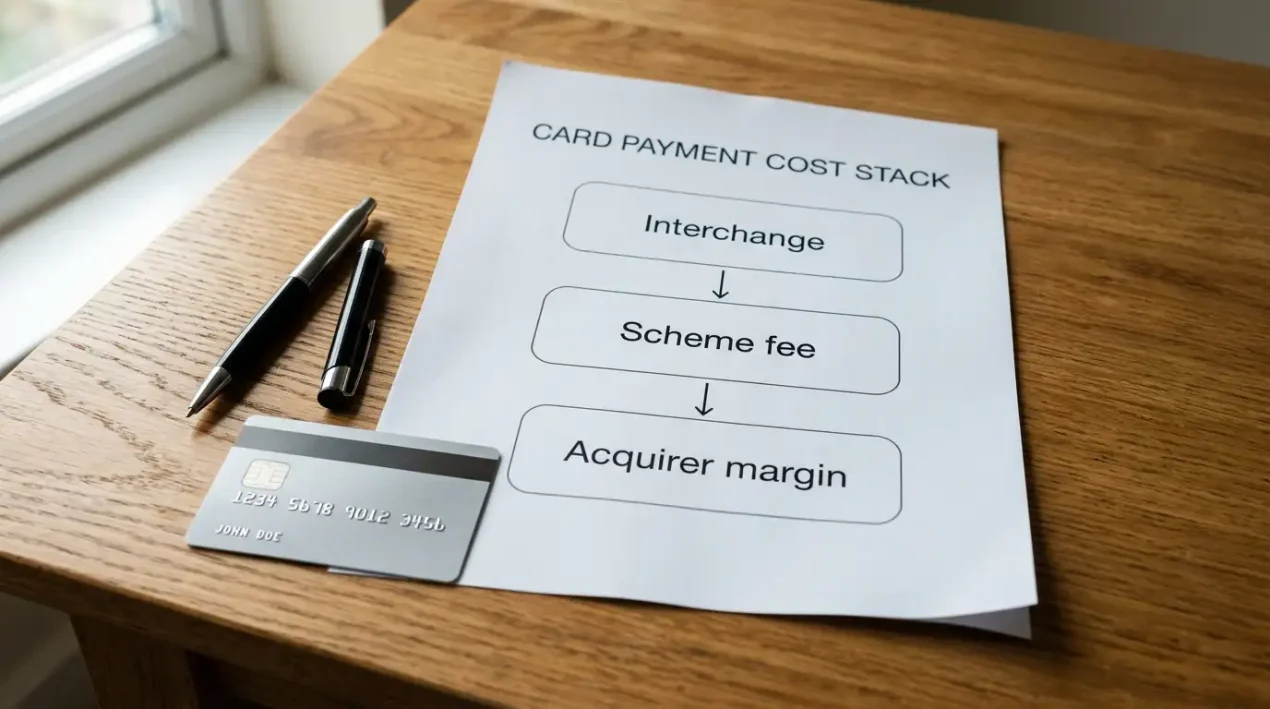

The card-payment cost stack from the bookmaker’s perspective

When an Australian bookmaker accepts a Visa Debit deposit, several distinct fees attach to that single transaction. The largest historically has been the interchange fee – paid by the merchant’s acquirer to the customer’s issuing bank – which compensates the issuer for handling the card account, providing fraud protection, and making the funds available. For a typical Visa Debit transaction in Australia before 2026, interchange ran around 8 to 12 basis points, or AU$0.08 to AU$0.12 per AU$100.

The next layer is scheme fees – paid by the merchant’s acquirer to Visa – which cover the cost of running the card network, settlement infrastructure, and brand maintenance. Scheme fees in Australia have historically been smaller than interchange, in the range of 5 to 8 basis points, but they’re billed across many sub-categories (cross-border fees, premium-card fees, fraud-monitoring surcharges) that can accumulate to more than the headline rate suggests.

The acquirer then adds its own merchant-service-fee margin on top of these wholesale costs, which is what the bookmaker actually sees on its monthly statement. For a high-volume operator with negotiating power, the all-in MSF on Visa Debit might run 0.4% to 0.7% of transaction value. For smaller operators with less leverage, 1.0% to 1.5% is more typical. That’s AU$4 to AU$15 of cost on every AU$1,000 of Visa Debit deposit volume, before anything related to the wagering itself.

How Australian Visa Debit interchange has been structured

The RBA has regulated card-scheme interchange for over a decade, capping the maximum rates that schemes can set for various transaction types. The pre-2026 caps for Visa Debit in Australia were set at levels that produced typical interchange of around 8 basis points on the regulated path. Premium cards – the various platinum and signature variants – had higher uncapped paths up until the regulatory framework caught up.

For wagering specifically, the interchange path was nothing special. MCC 7995 didn’t carry a separate interchange treatment under the RBA’s rules; it was treated identically to other consumer-debit transactions for fee purposes. So the 8-basis-point average applied to bookmaker deposits the same way it applied to grocery purchases.

What changes from 1 October 2026 is the cap structure itself. The RBA’s reform package lowers the maximum interchange rates on debit and credit transactions, with the explicit goal of reducing the cost of card acceptance and offsetting the elimination of merchant surcharging. The reform’s combined effect – lower interchange plus no surcharging – is intended to leave around 90% of Australian businesses better off.

The scheme-fees component and why it’s harder to track

Scheme fees are the most opaque part of the cost stack. Unlike interchange, which is publicly capped and disclosed by the RBA, scheme fees are set by the card brands themselves and aren’t subject to regulated rate disclosure. The fees include base transaction charges, but also per-attribute fees for things like premium cards, cross-border processing, fraud-mitigation services, tokenisation, and a long tail of optional features.

Visa is the dominant card brand globally – more than 3.3 billion cards in circulation in 2026, around 52.8% of all banking cards – and its scheme-fee schedule is correspondingly complex. For a typical Australian Visa Debit transaction at a bookmaker, the scheme fee combines a base rate, a transaction-type modifier, and any applicable surcharges for specific features. The total usually lands somewhere between 4 and 7 basis points, but the specifics can shift quietly when Visa updates its fee schedule.

For the punter, the scheme-fees layer is invisible – the customer pays the bookmaker, and the bookmaker pays the acquirer, and the acquirer settles with Visa. But for the operator, scheme fees are a meaningful component of card-acceptance cost, and operators with sophisticated payments teams negotiate hard on the elements they can influence (volume tiers, processing-method selection, tokenisation discounts).

The bookmaker’s MSF and where the margin sits

The merchant-service-fee is the all-in cost the bookmaker actually pays its acquirer for processing the deposit. It rolls up interchange, scheme fees, and the acquirer’s processing margin into a single rate. In Australia, the regulated interchange path means that competitive acquirers can offer a thin overall margin on top of pass-through costs, which keeps MSFs in check for high-volume operators.

Smaller operators have less bargaining power and pay higher MSF rates. A challenger licensee processing AU$50 million a year of card deposits might pay 1.2% to 1.5% MSF; a major operator processing AU$500 million might pay 0.5% to 0.7%. The differential is meaningful at industry scale – at higher volumes, a 1% difference in MSF is millions of dollars annually.

The compliance picture matters here too. The pre-creation verification rules from 29 September 2024 added KYC infrastructure that interacts with the payments stack – operators have to verify identity before any deposit, which adds a small but real cost to the customer-onboarding flow. The credit-card ban from 11 June 2024 also means operators can no longer accept credit-card deposits at all, with fines of up to AU$247,500 per breach for non-compliance, which has eliminated the higher-margin credit interchange path that previously offset some of the operator’s cost on debit transactions.

Who actually pays for all of this

The honest economic answer is that the customer pays, eventually, but indirectly. Bookmakers don’t surcharge Visa deposits in Australia – this was already true at most operators before the October 2026 reform formalised it – so the cost of card acceptance is absorbed into the operator’s overall pricing. That pricing shows up in the odds offered, the size of promotional bonuses, and the take-rate on various wagering products.

If interchange and scheme fees were AU$0, operators would have more headroom for sharper odds or bigger promotions. With interchange at 8 basis points and scheme fees at 5 basis points, that headroom is reduced by roughly 0.13% of deposit volume. The reform package’s interchange reductions free up some of that, which is part of why the RBA’s modelling suggests a net positive for both sides of the market.

“Around 90 per cent of Australian businesses are estimated to be better off under the proposed policies,” is how the RBA characterised the package, and that’s a meaningful statement at the system level. For wagering specifically, the operator captures the cost saving directly, and the question becomes how much of that gets reinvested in customer-facing competitiveness versus retained as operator margin.

The post-October 2026 picture

From 1 October 2026, the cost stack changes in two ways. Interchange caps drop, reducing the wholesale cost the operator’s acquirer pays the customer’s issuer. Surcharging is prohibited, removing the option to push card-acceptance cost back to the customer. The combined effect on a typical Visa Debit bookmaker deposit is that the operator pays less in interchange but has fewer levers to recover cost from individual customers.

For a competitive market like Australian wagering – over 90 licensed online bookmakers and around 134 active services in total – the savings will largely be passed back to customers through promotional spend rather than retained as operator margin. The competitive dynamics ensure that any cost-saving differential between operators gets competed away over time, and the customer-acquisition arms race continues to consume the available economic surplus.

Check for potential Visa surcharges in 2026 when depositing.

For the deeper picture of how the surcharge component of the reform plays out in betting, my piece on how the RBA’s October 2026 rules change Visa surcharges covers the surcharge mechanics specifically.

Is there a public schedule of interchange caps in Australia?

Yes. The Reserve Bank publishes interchange caps on its website and updates them when the regulatory framework changes. The caps cover Visa, Mastercard, and other regulated card schemes, with separate rates for credit and debit transactions. The October 2026 reform changes the cap levels but the public-disclosure model continues.

Do Visa premium-tier debit cards cost the bookmaker more?

Slightly, but the differential is smaller than for premium credit cards. Premium Visa Debit products (Platinum, Signature, Infinite tiers) carry marginally higher interchange than standard Debit, but the regulated cap structure narrows the gap considerably. For most operators the cost difference is too small to justify treating premium debit cards differently at the deposit screen.

Does Visa Direct (payouts) carry scheme fees too?

Yes. Visa Direct push-to-card transactions incur their own scheme fees and processing costs, typically billed to the originator (the bookmaker) rather than the recipient (the customer). The fee structure is different from inbound debit transactions but follows the same general pattern of interchange-equivalent and scheme-fee components. The operator absorbs these costs as part of providing fast payout functionality.