BNPL and Betting: The Credit-Card Ban Status

The instalment plan that never quite fitted

The question shows up in support inboxes and forum threads with surprising frequency: “Can I deposit at a bookmaker with Afterpay?” The hopeful subtext is that BNPL feels different from a credit card – there’s no plastic with a credit limit, no statement at the end of the month, no interest charge if you pay on time. People who’ve adopted Afterpay or Zip for retail spending naturally wonder whether it carries the same regulatory baggage when applied to gambling. The answer is that it does, and the regulators have been quite clear about why.

The trickier issue is that not everyone realises BNPL is included in the credit-card ban. The legislation talks about “credit and credit-related products”, and “credit-related” is doing the work that catches BNPL inside the ban’s perimeter. So this piece sits at the intersection of new payments behaviour and old regulatory boundaries – what BNPL is, why it’s classified the way it is, and which alternatives actually still work for Australian betting deposits in 2026.

Stay informed on this sports platform.

What the legislation actually says

“Australians should not be gambling with money they do not have. Last year, the Albanese Labor Government committed to banning credit cards for online wagering – and we’ve delivered.” That’s the framing the Minister for Communications used when the rules took effect on 11 June 2024, and it’s the interpretive lens the regulators have been applying ever since.

The actual statutory text in the Interactive Gambling Amendment (Credit and Other Measures) Act 2023 prohibits licensed Australian wagering operators from accepting payments via credit cards, credit-related products, and digital currencies. The penalty for breach is up to AU$247,500 per incident – substantial enough that operators don’t take the rule lightly.

The phrase “credit-related products” is what catches BNPL. The legislation didn’t enumerate every form of credit instrument the ban covers, partly because the payments market is too innovative to settle for a static list, and partly because the policy intent was to cover the underlying mechanism rather than specific brand names. If a payment instrument extends credit to the consumer – that is, if the consumer pays the merchant now using money the consumer doesn’t currently possess – the instrument is captured. BNPL fits that definition cleanly, regardless of the brand wrapping it.

Why BNPL counts as a credit product

The mental model people apply to BNPL is “I split the payment over four instalments, the merchant gets paid up front by the BNPL operator, I pay the operator back over six weeks.” That description is accurate. It’s also the textbook definition of a short-term consumer credit product. The fact that Afterpay didn’t traditionally call itself credit, and that Zip Pay sits in a slightly different category from Zip Money, doesn’t change the underlying mechanic.

Regulators around the world have been catching up to BNPL’s true nature for years now. Australia’s Treasury landed on extending consumer credit protections to BNPL providers under the National Credit Act in stages from 2024, with full coverage rolling in by mid-2026. That brought BNPL operators inside the regulated consumer credit perimeter for the first time. The sequence matters for the gambling ban because it formalised what was already true in substance – BNPL is credit, and the wagering ban’s “credit-related products” language captures it.

From an operator’s perspective, this isn’t a grey area. A licensed Australian bookmaker accepting an Afterpay-funded deposit faces the same penalty exposure as one accepting a Visa credit card, regardless of how the BNPL flow appears at the checkout. Most operators figured this out in the months before 11 June 2024 and pulled BNPL options from their deposit interfaces well in advance of the deadline.

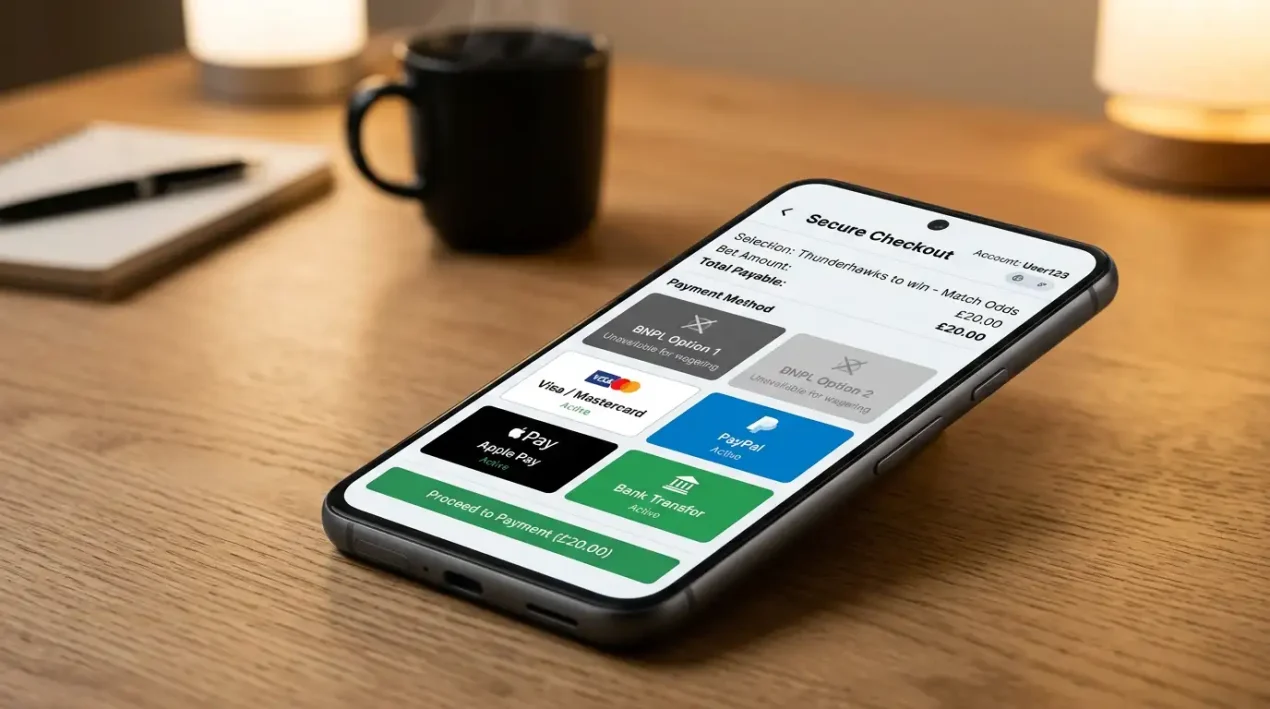

Current acceptance status across the major BNPL brands

The short version: none of the major BNPL operators are accepted at licensed Australian wagering sites for deposits, and that hasn’t changed since the ban took effect. Afterpay, Zip Pay, Zip Money, Klarna, Latitude Pay, Humm, PayPal Pay-in-4 and the smaller equivalents all sit outside the deposit-method options available to customers. Where they appeared in operator interfaces before 2024, they’ve been removed.

The same applies to BNPL options surfaced through digital wallets. If your Apple Pay or Google Pay configuration includes a BNPL card alongside debit and credit cards, the bookmaker reads the funding-source flag and refuses anything routed through the BNPL token. The fact that the wallet wraps multiple instruments inside one token doesn’t help – the funding-source classification travels through to the merchant, and BNPL flags get refused at the same checkpoint as credit-card flags.

The one place BNPL still appears in proximity to wagering is in the offshore market. Some unlicensed offshore operators continue to accept BNPL as a deposit method, banking on the fact that they’re not subject to Australian regulator oversight. About 36% of all online wagers placed by Australians now flow to offshore services, with channelisation falling from 74% in 2021 to 64% currently – a meaningful chunk of the market sits outside the ban’s effective reach. But routing BNPL through offshore wagering carries its own substantial risks beyond the deposit step itself.

Enforcement precedents and what the ACMA has been doing

The ACMA’s compliance reporting since the ban took effect tells the practical story of how the regulator has handled BNPL alongside other credit instruments. In a desktop review during March 2025, the regulator identified fifty licensed operators whose terms still mentioned credit cards or cryptocurrency as accepted methods – most of them outdated text rather than active acceptance, but the regulator required all fifty to update their disclosures by 30 June 2025.

The pattern that emerged from those reviews was that operators had broadly stopped accepting BNPL by the deadline, but the textual references in promotional and terms-of-service material lagged behind the operational change. The ACMA’s response was to push operators to align both layers – the actual payment routing and the customer-facing communication – so that customers couldn’t be misled into believing BNPL was an option.

In the broader 2024 to 2025 financial year, the ACMA opened ten new investigations and closed ten, including a AU$1 million fine plus mandatory two-year independent review for one operator. None of the public enforcement actions specifically named BNPL as the trigger, but the broader pattern is clear: the regulator is reading every layer of the payment funnel, and operators that left BNPL pathways open would be caught.

Why people still ask

The question keeps coming up partly because BNPL feels intuitively different from credit. It doesn’t carry interest if paid on time, it doesn’t show up as a credit-bureau line item the same way credit cards do, and the marketing has spent years emphasising “buy now, pay later” rather than “borrow now, repay later”. So people have absorbed BNPL as a budgeting tool rather than a credit instrument, and they expect it to be treated accordingly.

The other reason is that some BNPL providers do have debit-equivalent products in their broader portfolios. Zip operates Zip Pay (BNPL, captured by the ban) and other instruments that route differently. PayPal sits across multiple funding-source classifications depending on the user’s underlying wallet configuration. The ambiguity at the brand level lets users hold onto the hope that their particular configuration might escape the ban – which it generally doesn’t, but the perception persists.

The clean test isn’t the brand name – it’s whether the funding source represents money you have or money you’ll have to pay back. If you’re funding the deposit from a balance you’ve already accumulated (a debit card, a bank transfer, a fully-funded prepaid card, an Osko payment), it’s allowed. If you’re funding the deposit from a credit line, an instalment plan, or any “pay later” mechanism, it’s caught by the ban regardless of the brand wrapping.

Safer alternatives that actually work

For BNPL users looking for a similarly low-friction deposit option that complies with the rules, the practical alternatives are well-established. PayID over the New Payments Platform is the closest match – it’s mobile-first, requires no card details at the checkout, and settles in seconds. The processing speed is comparable to BNPL’s instant approval, and the funding source is your own bank balance rather than a credit line.

Standard Visa Debit also remains a clean option if you prefer the card-based experience. Linked to a transaction account that holds the funds you actually want to deposit, it provides scheme-level fraud protection, recognised dispute rights, and acceptance at every licensed Australian bookmaker. The fact that it doesn’t offer instalment splitting is the entire point – the legislation is designed to ensure deposits come from money the customer currently has, not money they’re scheduling to find.

For users who specifically value the budgeting discipline that BNPL provided, the better tool is an operator-level deposit limit set under the National Consumer Protection Framework. Setting a weekly or monthly deposit cap caps your wagering activity at a level you’ve decided in advance, which mimics the budgeting effect BNPL imposed without involving credit at all. The detailed mechanics of how those limits work in practice are covered in the deposit-limit analysis.

What this means for your wallet setup

If you’ve been using BNPL routinely for retail purchases, the cleanest setup for wagering is to keep BNPL out of the workflow entirely. That means making sure your default payment method at any bookmaker isn’t a digital wallet that could route through a BNPL card you’ve added for other purposes. The simplest path is to nominate a specific bank-issued Visa Debit or PayID identifier as your wagering payment method, and avoid the wallet-based ambiguity altogether.

This is closely related to the ban on credit card betting.

The setup discipline pays off later. If you ever scale up your activity and bump into the AUSTRAC AU$5,000 daily threshold, the operator’s enhanced due diligence is going to look at your funding sources. Having a clean trail through bank-issued debit instruments produces a faster verification touchpoint than a mixed history that includes ambiguous wallet routings. The cleaner the audit trail, the faster the recovery when anything does go sideways.

Can I link a BNPL account to a Visa Debit and use that at a bookmaker?

No. Even when BNPL providers issue an associated Visa Debit-style card for retail use, the funding source remains the BNPL credit line, and the bookmaker’s BIN classification reads the card as credit-related rather than as standard debit. The deposit will be refused at the same checkpoint as a direct credit-card transaction.

Did any bookmakers ever accept Afterpay before the ban?

A small number of operators experimented with BNPL acceptance in the 2021 to 2023 window, when the regulatory boundary around BNPL was less clear. Those experiments were short-lived and were comprehensively unwound before the credit-card ban took effect on 11 June 2024. There’s no licensed Australian operator currently accepting BNPL for deposits.

What happens if a bookmaker accepts BNPL by mistake?

The operator faces a regulatory breach with penalties up to AU$247,500 per incident. In practice modern operator gateways pre-screen for BNPL routing and refuse such transactions before they reach the deposit confirmation, so genuine accidental acceptance is rare. If it ever does happen, the operator is more likely to reverse the transaction and refund the customer than risk being caught by an ACMA review.